Let’s talk about this buzzword you’ve likely heard tossed around at industry meetings ‘social inflation.’ At its core, it’s about those skyrocketing insurance claim costs we’re all wrestling with, thanks to our society’s ever evolving whims and values. Think of it as the inflation of expectations and entitlements, where everyone’s trying to get a bigger slice of the pie. So, what’s driving these changes, and how does it impact your bottom line? Let’s dive in.

It’s like this, when insured parties are suing insurers, and courts of law keep giving out larger cash awards, we end up paying more to settle these claims. This drives up the Social Inflation, which in turn increases everyone’s insurance premiums and it’s especially noticeable in personal injury cases.

Source: How legal system abuse drives social inflation

Unmasking Social Inflation: Decoding its Impact and Strategizing Your Defense in the Insurance Industry

Alright, let’s analyze it in the nitty-gritty by uncovering the true financial impact of inflation on your insurance company with hard data that directly affects your bottom line. These historical figures on social inflation trends can illuminate how much these social inflation drivers ramp up your loss costs.

Consider the rise in attorney advertising and litigation funding. Quantifying the impact of new plaintiff attorney strategies and the practice of phantom billing can be trickier. However, the strongest evidence comes from the skyrocketing court awards. Here’s what the data tells us:

- New figures from the Insurance Times reveal that motor insurers faced significant and sustained cost pressures in 2023, with repair costs rising by 31% in just one year. On average, insurers paid out £1.13 million every hour in claims. Feeling the squeeze yet?

- Remember the infamous 1994 McDonald’s $2.7 million hot coffee lawsuit? It was a product liability case that grabbed headlines and fueled social inflation. This case highlighted how high-profile lawsuits can ripple through the industry, affecting insurers like you.

- The American Transportation Research Institute (ATRI) found that from 2010 to 2018, the size of court verdicts against trucking companies shot up by 51.7% per year. Compare that to standard inflation and healthcare costs, which grew at just 1.7% and 2.9%, respectively. The average verdict size for trucking accidents over $1 million rose from $2.3 million to $22.3 million in that period. That’s a tenfold increase—mind-blowing, right?

- Closer to home, New York City’s Metropolitan Transit Authority (MTA) saw personal injury payouts rocket from $43 million in 2007 to $150 million in 2019. MTA attorney Lawrence Heisler pointed out how the pandemic has exacerbated this issue, with courts being swayed by ‘anchoring’—where counsel asks for sky-high awards, leading to jury decisions that are far from reasonable.

- VGM Insurance found that the median cost of a single-fatality award in 2001 was $1.45 million. By 2015, it had only inched up to $2.0 million. But then it skyrocketed to $3.85 million by 2020. If it had risen at the rate of inflation, it would have been around $2.25 million. Instead, it rose at nearly twice that rate.

These are not just numbers, they’re the wake-up calls. Understanding these trends helps you anticipate potential increases in claims, allowing you to adjust your pricing and risk management strategies accordingly. By staying informed and prepared, you can better navigate the challenges posed by social inflation. So, let’s roll up our sleeves and tackle these hurdles together!

Impact of Inflation on Insurance

Litigation Trends: Almost every week, you probably hear law firms boasting about the millions of dollars in suits they filed against insurance companies, and courts are handing out larger settlements. This directly impacts you as an insurance company because it means you have to pay more to settle these claims. This, in turn, bumps up the overall cost of your claims, and to compensate for that loss, you raise insurance premiums across the board.

The trend doesn’t stop there. Higher jury awards and a shift in jury composition are also part of it. The changing demographics of your jury pool can influence how cases are seen and awarded. It’s a changing landscape, and as an insurance company, understanding these trends will help you navigate the future.

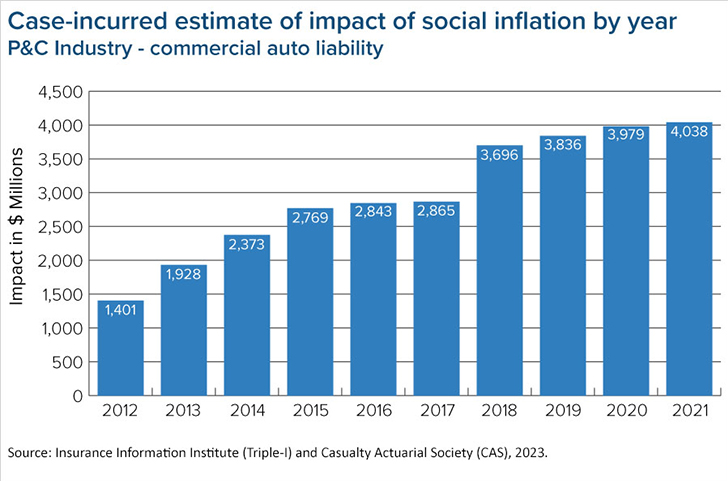

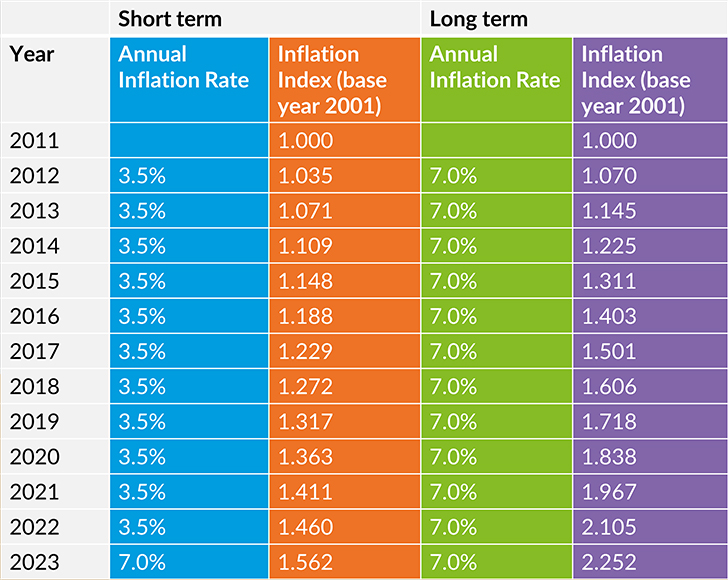

Source: ANA_Social_Inflation_and_Insurance_Industry_Blog_Graphics2-min.jpg

Source: ANA_Social_Inflation_and_Insurance_Industry_Blog_Graphics2-min.jpg

Cultural Shift: Have you noticed a shift in public opinion? People are increasingly holding corporations responsible for societal issues. This could mean more claims against your insured companies. For example, if a company is perceived as not doing enough to fight climate change, it might face more claims. This would drive up your overall insurance cost.

This shift involves a broader understanding of liability – the unfulfilled obligations between parties. People increasingly believe that someone should pay when there’s damage or injury, regardless of negligence.

And then there’s the public distrust of corporations. This skepticism towards big businesses can tip the scales in favor of the plaintiffs, no matter how much or how little your insured company might be at fault. These cultural shifts can significantly impact your operations, so staying ahead is key.

Another factor is the public’s growing mistrust of corporations. People who are suspicious of big businesses might side with the plaintiff, regardless of whether the defendant is at fault.

Media Influence: How can we forget about the media? If news outlets and social media portray large insurance payouts as a good thing, naturally, it creates the impression that anyone can file a claim and get a big payout. This perception has led to a surge in the number and size of claims, hiking up the Social Inflation. Even radical ideas can spread like wildfire on social media, shaping people’s views on certain issues.

The media plays a big role in shaping public opinion. Have you noticed how it often paints large insurance payouts in a positive light? This can lead people to believe they, too, can file a claim and land a huge payout. The result? Increasing the number and size of claims drives your insurance costs up. Media portrayals can make it seem like these big jury awards are the norm, leading juries to believe that defendants, especially larger corporations like yours, can easily afford to pay bigger sums. This is something to watch, as it can significantly impact your bottom line.

Both traditional media outlets and social media are involved in this. They’re powerful drivers of social inflation, even capable of spreading extreme ideas and opinions. This shapes attitudes and perceptions towards various issues.

Source: How future claims cost may be impacted by inflationary pressures

Implement Effective Cybersecurity for Insurance Companies and Avoid Data Breaches and the Costly Penalties!

Taking Social Inflation by its Horns

When the economy takes a downturn, you’ve likely noticed more people turning to litigation as a quick way to make money. This mindset can lead to a surge in claims, driving up insurance costs across the board. To stay ahead of this, it’s crucial to implement proactive strategies:

The Role of Legal Technology and Analytics

Have you noticed how quickly technology advances in the legal field? The leaps and bounds in technology, marketing, and analytics in the legal field are spurring this trend on. Legal firms are using sophisticated analytics to identify and pursue lucrative cases. This can contribute to an increase in claims and higher payout expectations. Staying updated on these advancements and understanding their implications is key to navigating the choppy waters of social inflation.

Regulatory Changes: What to Watch

Let’s not forget about the ever-evolving laws and regulations. These changes can sometimes allow people to sue companies more easily, leading to an uptick in claims. Imagine if a new law lowers the hurdles for plaintiffs in lawsuits, we might see more successful claims against companies, causing a spike in the cost of insurance claims. Keeping a close watch on regulatory developments and being prepared to adapt your strategies accordingly is essential.

Strengthen Your Case with Proof

The proof is essential to navigating social inflation, so let’s explore how you can effectively prove your preparedness and strategies.

Strengthening Underwriting Practices

One way to combat the effects of social inflation is by beefing up your underwriting standards. Conducting thorough risk assessments and implementing stricter underwriting standards can help you spot potential vulnerabilities. For instance, rather than a general assessment, laser-measured metrics should be used to evaluate risks specific to each policy, similar to how some companies offer precise fittings for specific car models.

Enhancing Claims Management

Efficient claims management can also play a vital role. Implementing robust claims handling procedures and training your team to identify fraudulent or exaggerated claims can help control costs. Leveraging advanced analytics to predict and manage claims trends provides valuable insights for better decision-making. Think of it like using a demo of your product to show its effectiveness—here, you’re demonstrating your ability to handle claims efficiently.

Fostering Strong Relationships with Legal Partners

Building and maintaining strong relationships with experienced legal partners is crucial. A knowledgeable legal team can provide invaluable support and help you develop robust defense strategies. Pointing to third-party endorsements, like reputable legal firms supporting your case, can be as persuasive as testimonials or third-party reviews in the consumer world.

Advocating for Legal Reforms

Pushing for legal amendments to combat social inflation is another strategy. You could advocate for stricter rules on litigation funding or tighter caps on pain-and-suffering damage awards. Just like social proof can be persuasive in marketing—showing industry-wide support for these reforms can strengthen your position.

By getting to grips with the driving forces behind social inflation, you’ll be well-positioned to anticipate potential increases in claims. This knowledge will enable you to effectively tweak your pricing and risk management strategies. Remember, we’re all in this together, so let’s roll up our sleeves and face these challenges head-on!

Cushioning the Impact of Inflation on Insurance with Outsourcing

Navigating the choppy waters of social inflation and evolving regulations can feel overwhelming, right? But here’s some good news—outsourcing to Insurance Backoffice Pro can solve these challenges for you. With over 15 years of experience in the American insurance industry, we offer top-notch back-office support designed to reduce the impact of social inflation on your business.

Imagine having a team of seasoned experts who truly get the ins and outs of the insurance landscape working alongside you. We help you streamline operations, cut costs, and boost efficiency so you can focus on what you do best. By partnering with us, you’ll be in a prime position to anticipate and manage potential increases in claims effectively.

Ready to take your insurance services to the next level and make your business more resilient? Contact Insurance Backoffice Pro today and let’s roll up our sleeves and tackle these challenges together!

Prev

Prev